Why geopolitical fragmentation is changing the way financial models are built

For decades, globalization did more than reshape supply chains and international trade. It also simplified the assumptions behind modern financial modeling.

Businesses operated in an increasingly interconnected world where capital moved relatively freely, trade barriers declined, supply chains became globally optimized and geopolitical friction remained comparatively contained. As a result, many financial models evolved around a similar implicit assumption: that the world was converging economically, operationally and, to some extent, politically.

That assumption is becoming increasingly difficult to sustain.

Today’s environment is shaped by regionalization, industrial policy, strategic autonomy, export controls, tariff uncertainty and growing geopolitical competition between major economic blocs. The implications are not only macroeconomic. They directly affect how businesses should be modeled, valued and forecasted.

In many cases, the issue is no longer whether a model is “complex enough”, but whether its assumptions still reflect the structure of the world it is trying to represent.

Globalization quietly simplified financial modeling

One of the less discussed consequences of globalization was the reduction of structural friction.

For years, many companies could assume:

- relatively stable trade relationships,

- globally optimized supply chains,

- predictable access to manufacturing hubs,

- expanding international markets,

- and a gradual convergence in operational efficiency.

This created a modeling environment where global averages often worked reasonably well. Revenue growth assumptions, margin structures, sourcing strategies and capital allocation decisions could frequently be modeled with a relatively unified framework.

A company manufacturing in Asia and selling into Europe or the United States was not necessarily viewed as carrying major structural geopolitical risk. Efficiency was the dominant assumption.

But the world is becoming less homogeneous.

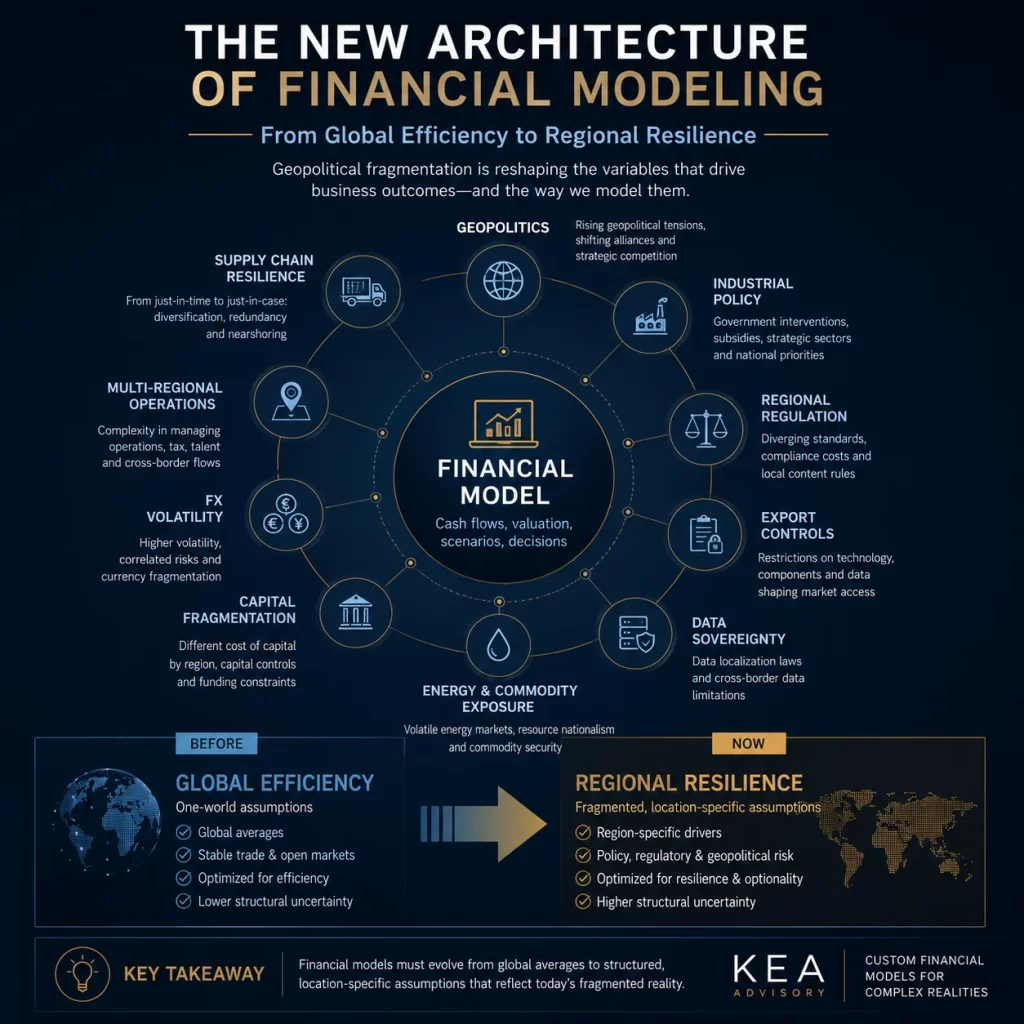

Increasingly, businesses must operate across different political priorities, regulatory environments and strategic interests. As this fragmentation grows, financial assumptions become more localized, more conditional and less transferable across geographies.

In other words, globalization made many financial models cleaner. Fragmentation is making them more representative of reality.

The rise of fragmented assumptions

This shift is already visible across industries.

Apple, for example, has spent years diversifying part of its manufacturing footprint beyond China toward countries such as India and Vietnam. That decision is not simply operational. It reflects a broader need to reduce concentration risk and increase geopolitical resilience.

From a modeling perspective, that changes several assumptions simultaneously:

- capital expenditure requirements,

- manufacturing efficiency,

- logistics costs,

- working capital needs,

- and potentially even long-term margin expectations.

Similarly, ASML has become increasingly exposed to export restrictions linked to semiconductor technology and geopolitical tensions. In that context, forecasting future revenue is no longer driven solely by market demand or technological leadership. Political decisions themselves become part of the forecasting framework.

The same applies to NVIDIA, where demand for AI infrastructure may remain structurally strong while export controls simultaneously limit access to certain markets. A traditional “global demand” assumption becomes less useful when access to that demand is politically constrained.

Meanwhile, TSMC illustrates another increasingly important issue: geographic concentration risk. A highly efficient global supply chain may still represent a structural vulnerability if critical production capacity is concentrated in strategically sensitive regions.

These examples may appear specific to large multinational corporations, but the underlying logic increasingly applies across mid-sized companies, startups and international businesses as well.

A European software company expanding internationally may face different data localization requirements across regions. A manufacturer may need to duplicate suppliers to improve resilience. A business previously optimized for efficiency may now prioritize redundancy, regional diversification or regulatory adaptability.

All of those decisions affect financial models.

Why traditional modeling frameworks are under pressure

The challenge is not that traditional financial modeling techniques are obsolete. Discounted cash flow analysis, forecasting methodologies and valuation frameworks remain fundamentally useful.

What is changing is the stability of the assumptions underneath them.

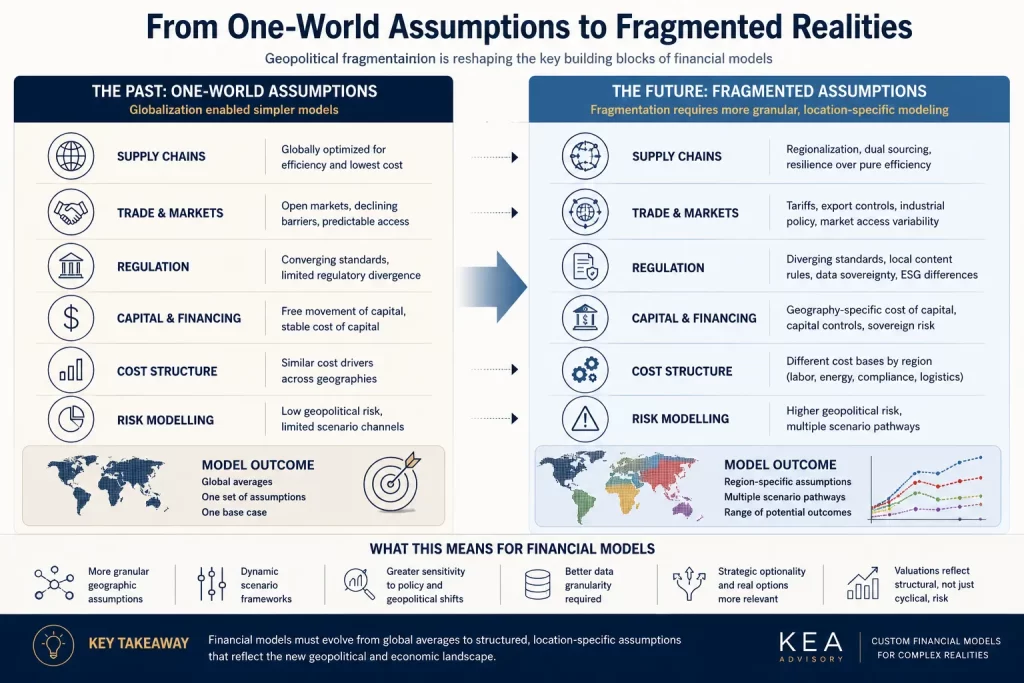

Historically, many models implicitly relied on:

- stable globalization,

- low geopolitical friction,

- predictable supply chains,

- and relatively uniform access to markets and capital.

Today, those assumptions often require greater segmentation.

Margins may differ materially by geography. Regulatory costs may vary significantly between jurisdictions. Supply chain resilience may require duplicated infrastructure or higher inventory levels. Tariffs and industrial policy can alter competitive positioning. Country risk may become more dynamic even within developed markets.

Increasingly, “global averages” are becoming less representative.

This does not necessarily mean every model must become dramatically more complicated. In fact, complexity for its own sake often reduces clarity.

But it does mean that financial models increasingly need to incorporate structural fragmentation more explicitly:

- region-specific assumptions,

- geopolitical sensitivity,

- regulatory divergence,

- supply chain dependencies,

- and multiple operational pathways.

For years, efficiency was one of the dominant modeling assumptions. Increasingly, resilience is becoming one too.

Financial modeling in a more fragmented world

This shift also has important implications for advisory work and decision-making.

Businesses are no longer operating in a purely economic environment. They are operating within overlapping systems of politics, regulation, technology and strategic competition. As a result, financial modeling increasingly becomes an exercise in translating geopolitical and operational realities into financial assumptions.

That requires models capable of adapting to more fragmented environments rather than relying on overly standardized global frameworks.

The goal is not to predict geopolitics. It is to recognize that geopolitics is increasingly influencing financial outcomes directly.

In many ways, the era of “one-world financial modeling” is ending.

The next generation of financial models will likely be less dependent on universal assumptions and more focused on structural adaptability, regional specificity and operational resilience.

And increasingly, businesses will require custom-built models capable of reflecting that reality rather than simplifying it away.