The potential IPO of SpaceX is shaping up to be one of the most anticipated—and complex—public offerings in modern financial history. With valuation estimates ranging between $150 billion and $200+ billion in recent secondary transactions, the transaction could become one of the largest IPOs ever.

However, beyond the headlines, the key question for investors is not whether the IPO will be large—but whether it will be properly understood, realistically valued, and ultimately investable.

1. Understanding the SpaceX Business Model

SpaceX is not a single business—it is a combination of distinct but interconnected activities:

A. Launch Services (Core Business)

SpaceX’s original activity, launched in 2002, consists of designing, manufacturing, and launching reusable rockets (Falcon 9, Falcon Heavy, Starship).

- Customers:

- Government agencies (primarily NASA and the U.S. Department of Defense)

- Commercial satellite operators

- International space agencies

- Geography:

- Launch sites in the United States (Florida, Texas, California)

- Global customer base

- Business model:

- Per-launch contracts (typically $50M–$100M per Falcon 9 launch)

- Long-term government programs (e.g., crewed missions, lunar programs)

- Financial profile (indicative):

- Lower margins relative to software businesses

- Capital-intensive but increasingly efficient due to reusability

This segment resembles aerospace & defense, typically trading at lower multiples.

Relevant comparables include:

- Rocket Lab

- Northrop Grumman

- Lockheed Martin

B. Starlink (Satellite Internet Business)

Launched commercially in 2019, Starlink provides global broadband internet via a constellation of low Earth orbit satellites.

- Customers:

- Consumers (residential broadband)

- Businesses (remote operations, maritime, aviation)

- Governments (connectivity in conflict zones and remote regions)

- Geography:

- Active in 60+ countries, including the US, Europe, Latin America, and parts of Africa

- Business model:

- Monthly subscription (~$90–$120)

- Hardware sales (terminals)

- Financial profile (estimated):

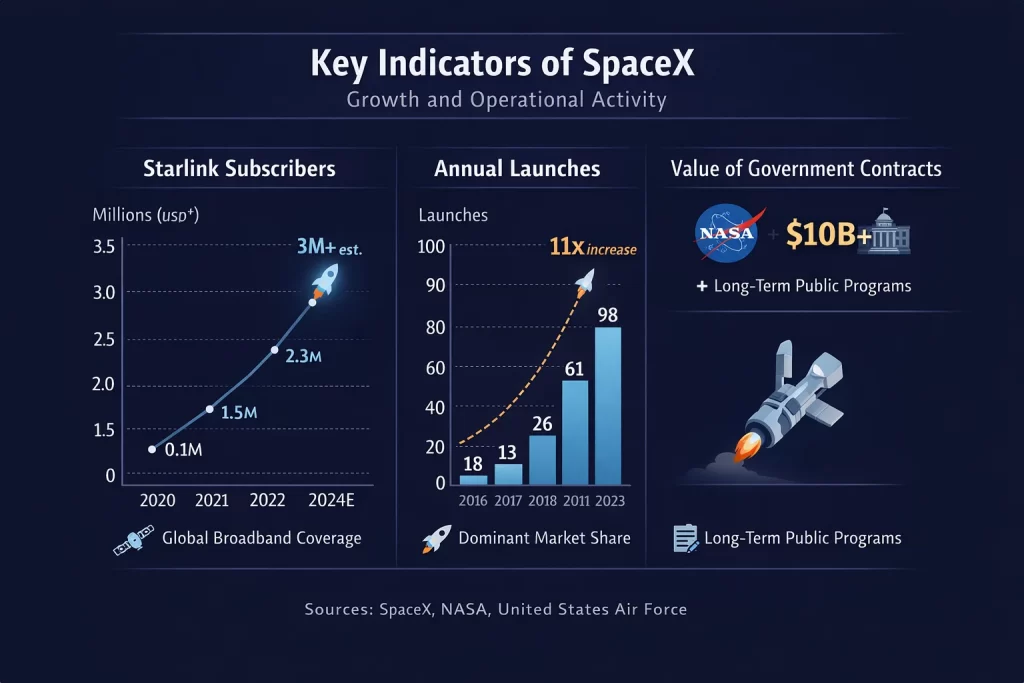

- Revenue estimated at $6–8 billion (2025–2026)

- Subscriber base exceeding 3 million users globally

- Higher-margin, recurring revenue profile

This segment is structurally closer to telecom + SaaS-like recurring models.

Relevant comparables include:

- Iridium Communications

- Viasat

C. Optionality (Starship, AI, Infrastructure)

Beyond its current businesses, SpaceX embeds significant future optionality:

- Starship → potential disruption in space logistics and cost structure

- Defense and intelligence applications

- Integration with AI ecosystems (e.g., data infrastructure, satellite-based compute)

This portion of the valuation behaves more like venture capital embedded in a mature company.

2. Where Do the Valuation Estimates Come From?

Unlike public companies, SpaceX does not publish financial statements. Valuation estimates are derived from:

A. Secondary Market Transactions

SpaceX shares trade privately through tender offers and secondary platforms.

- Recent transactions (2023–2025) have implied valuations of:

- ~$137 billion (2023)

- ~$175–180 billion (late 2024 / early 2025)

These transactions are often driven by:

- Employee liquidity events

- Institutional demand

Important: these are not fully price-discovery markets, but they provide the most reliable valuation anchors available.

B. Analyst Estimates

Banks and research firms build models based on:

- Launch cadence (number of missions per year)

- Starlink subscriber growth

- ARPU assumptions

- Industry benchmarks

These models are highly assumption-driven, particularly for Starlink and future businesses.

C. Government Contract Disclosures

Public information includes:

- NASA Commercial Crew contracts (~$4–5 billion total program value)

- NASA Human Landing System (Starship) contract (~$2.9 billion initial award, with extensions)

- U.S. Department of Defense launch contracts (multi-billion framework agreements)

These provide visibility on baseline revenue and credibility, but not full financial transparency.

3. How Should SpaceX Be Valued?

A. Sum-of-the-Parts (SOTP) as the Primary Framework

Given the diversity of businesses, SOTP is the most appropriate approach:

- Launch → aerospace multiples (lower)

- Starlink → telecom / growth multiples (higher)

- Optionality → venture-style valuation

Key insight: a large portion of value comes from future expectations rather than current earnings.

B. Why a Traditional DCF Is Structurally Weak Here

A standard DCF assumes:

- Predictable cash flows

- Stable reinvestment needs

- Reasonable terminal visibility

SpaceX does not meet these conditions:

- Highly uncertain long-term cash flows

- Massive and variable capital expenditure

- Significant dependency on breakthrough technologies

Therefore, a DCF can be built—but:

- It is extremely sensitive to assumptions

- It risks creating a false sense of precision

In practice, it should only be used as a scenario tool, not as a primary valuation anchor.

C. Market-Based Valuation and “Narrative-Driven Assets”

SpaceX is better understood as a narrative-driven asset.

This means valuation is driven by:

- Belief in long-term dominance

- Strategic positioning

- Market storytelling (space economy, global connectivity, AI infrastructure) rather than near-term financial metrics.

4. What Information Is Actually Available?

Despite being private, several data points are available:

A. Secondary Market Signals

- Valuation range: ~$137B → ~$175B+

- Strong institutional demand

B. Starlink Growth Indicators

- Subscribers: >3 million

- Revenue: ~$6–8 billion estimated

- Rapid expansion across continents

C. Launch Activity

- ~90+ launches annually (recent cadence)

- Dominant global market share

D. Government Backlog

- Multi-billion dollar contracts

- Long-term program visibility

However, critical gaps remain:

- Segment-level profitability

- Consolidated margins

- True free cash flow

This creates a familiar IPO pattern:

High narrative clarity, limited financial transparency

5. Recent IPOs: What Does the Market Really Tell Us?

To properly frame a potential SpaceX IPO, it is essential to look beyond the company itself and examine how recent IPOs—particularly in technology and capital-intensive sectors—have behaved.

Over the past few years, the IPO market has shown a clear pattern. Companies tend to go public during windows of strong investor demand, often supported by compelling narratives and optimistic forward projections. At listing, this typically translates into strong initial demand and premium pricing, especially for businesses positioned around transformative themes such as artificial intelligence, energy transition, or, in this case, the space economy.

However, once the initial enthusiasm fades and more data becomes available, a second phase begins. Investors shift their focus from narrative to fundamentals: revenue quality, margin structure, capital intensity, and execution. This transition often leads to increased volatility, particularly after lock-up periods expire and early investors begin to exit.

In capital-intensive sectors, this dynamic is even more pronounced. Companies that require continuous reinvestment—whether in infrastructure, hardware, or R&D—are more difficult to value purely on growth expectations. As a result, many IPOs in these segments experience a gradual “recalibration” of valuation as markets gain a clearer understanding of their economic reality.

In this context, SpaceX would not be an exception—it would likely be an amplified version of this pattern.

6. Sector Implications: The “Space Economy” Effect

A SpaceX IPO would not only be a company-specific event—it would act as a catalyst for the entire space sector.

When a market leader becomes publicly listed, it effectively establishes a benchmark. Investors gain a reference point for valuation, growth expectations, and capital allocation within the industry. In the case of SpaceX, this could significantly reshape how the so-called “space economy” is perceived.

On one hand, the IPO could unlock substantial investor interest in adjacent companies. Businesses such as Rocket Lab or AST SpaceMobile could benefit from increased visibility and capital inflows, as investors look for alternative ways to gain exposure to the sector.

On the other hand, SpaceX’s sheer scale and strategic positioning could have the opposite effect. By concentrating attention and capital, it may raise the competitive bar and make it more difficult for smaller players to justify their valuations unless they can demonstrate clear differentiation.

Ultimately, the IPO could redefine the sector along two axes: those with scalable, commercially viable models—and those still reliant on long-term, uncertain technological breakthroughs.

7. Warren Buffett’s Perspective: A Timeless Framework

Warren Buffett has consistently expressed caution regarding IPOs.

His well-known remark that “IPOs are sold, not bought” captures a fundamental truth about how these transactions are structured. Companies typically choose to go public when market conditions are favorable, investor appetite is strong, and valuations can be maximized. In other words, the timing is rarely neutral—it is strategic.

This does not imply that IPOs are inherently poor investments. Rather, it suggests that they often embed a level of optimism that may not fully reflect future risks or execution challenges.

Buffett’s approach, implicitly, is one of patience and discipline. Instead of participating in the initial offering, he prefers to wait until the market has had time to digest the business, reassess expectations, and establish a more stable pricing range.

Applied to a case like SpaceX, this perspective becomes particularly relevant. When a company combines technological ambition, strong narrative appeal, and limited financial transparency, the risk of overpaying for future potential increases significantly.

The key question is not whether the company is exceptional—but whether the price paid already assumes that it will be.

8. Key Risks: Looking Beyond the Narrative

In a transaction of this magnitude, risk does not come from a single source—it emerges from the interaction between valuation, execution, and market psychology.

The most immediate risk lies in valuation itself. When a company is priced based on long-term expectations rather than current cash flows, even small changes in assumptions—growth rates, margins, capital intensity—can lead to significant differences in implied value.

Execution risk is equally important. SpaceX operates at the frontier of multiple industries, where success depends not only on demand but also on technological reliability, regulatory frameworks, and the ability to scale complex infrastructure. Delays, cost overruns, or underperformance in any of these areas could materially impact the investment case.

At the same time, the company’s capital intensity introduces an additional layer of complexity. Unlike asset-light businesses, SpaceX requires continuous and substantial reinvestment. This creates tension between growth and free cash flow generation—an issue that markets tend to reassess over time.

Finally, there is the role of market sentiment. High-profile IPOs often attract investors driven as much by narrative as by fundamentals. While this can support valuations in the short term, it also increases the risk of volatility as sentiment shifts.

Taken together, these factors reinforce a central idea:

understanding SpaceX as an investment requires going beyond the story—and rigorously analyzing the assumptions that sustain it.

Final Thought

In situations like this, structured financial analysis becomes essential. Breaking down the business into components, stress-testing assumptions, and building flexible valuation frameworks allows investors to move beyond narrative and make informed decisions—even in the absence of complete information.