At first glance, a company’s valuation in the stock market seems simple: it is the share price multiplied by the number of outstanding shares. Yet this apparent simplicity hides a far more complex reality. Market valuation is not just a number—it is the result of expectations, financial performance, risk, and human behavior interacting continuously.

One of the most important distinctions in valuation is the difference between price and value. As Warren Buffett famously said, “Price is what you pay; value is what you get.” This idea captures the essence of investing. The market price reflects what investors are currently willing to pay, but intrinsic value reflects what a company is actually worth based on its future ability to generate cash.

Understanding why price and value diverge leads to a deeper question: how efficient are markets?

Perfect vs. Imperfect Markets

In theory, financial markets can be perfectly efficient. Under the Efficient Market Hypothesis, developed by Eugene Fama, prices fully reflect all available information.

However, even within this framework, Fama’s later work—and subsequent academic research—recognized that returns are not explained by a single factor alone. This led to the development of multi-factor models that help explain why some assets systematically trade at different valuations.

Among the most relevant factors are:

- Size (SMB – Small Minus Big): Smaller companies tend to offer higher expected returns, partly due to higher perceived risk and lower analyst coverage.

- Value (HML – High Minus Low): Companies with lower valuation multiples (so-called “value stocks”) often outperform growth stocks over time, reflecting market mispricing or risk premium.

- Profitability and Quality: Firms with stronger margins and more stable earnings profiles tend to command higher valuations.

- Investment Intensity: Companies that reinvest aggressively may carry different risk-return profiles compared to more conservative businesses.

- Liquidity Risk: Less liquid assets typically require a return premium, as they are harder to trade without impacting price.

These factors help explain why markets are not perfectly “flat” or uniform, even if information is broadly available.

In practice, however, markets are not perfectly efficient.

Information is unevenly distributed, investors interpret data differently, and behavioral biases influence decision-making. Insights from Behavioral Finance show how overconfidence, herding, and sentiment can drive prices away from intrinsic value.

This is where the distinction between theoretical efficiency and real-world imperfections becomes critical.

The Foundation: Financial Fundamentals

At the core of valuation lies the economic reality of the business. Revenues, margins, and cash flow generation determine long-term value creation.

Yet valuation is forward-looking. Expectations around growth, scalability, and competitive advantage often matter more than current performance.

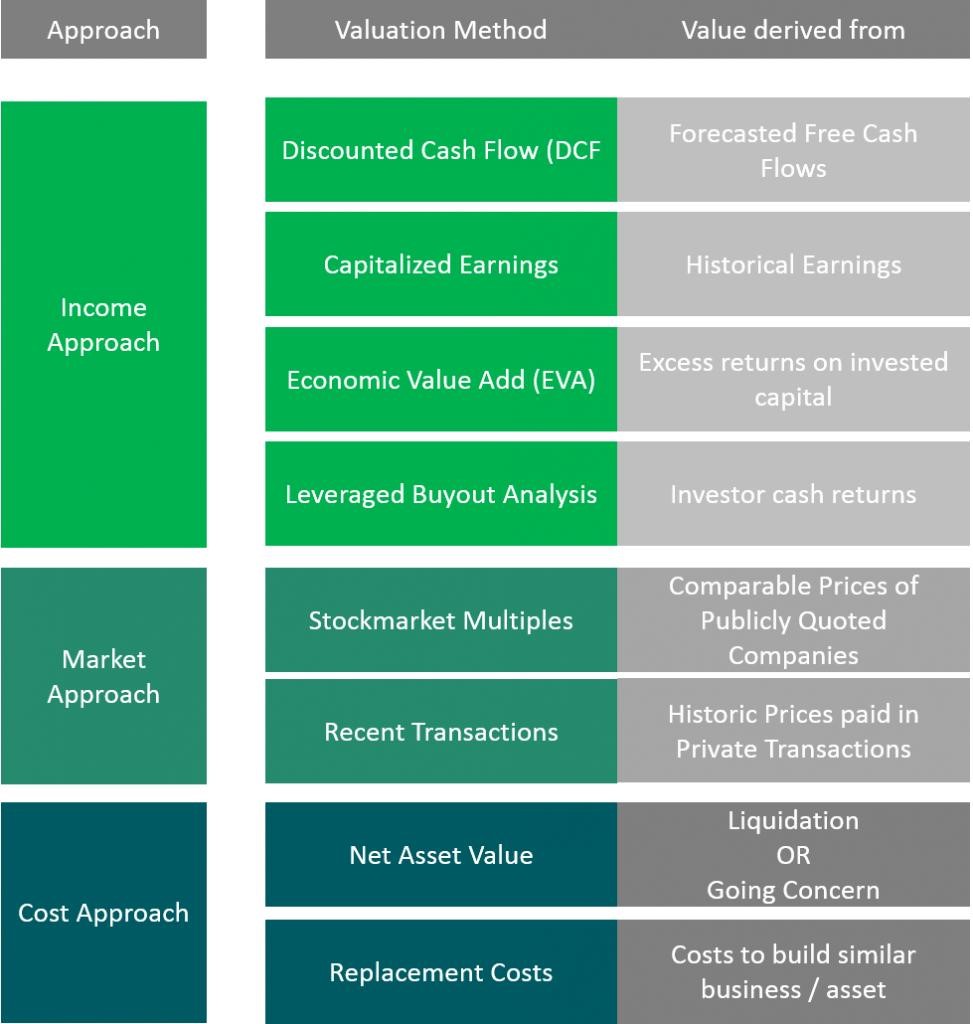

Intrinsic Value: A Structured Approach

The Discounted Cash Flow (DCF) method provides a theoretically grounded estimate of intrinsic value by projecting future cash flows and discounting them for risk and time.

It answers a fundamental question: what should this business be worth, based on its ability to generate cash?

But in imperfect markets, no single method is sufficient.

Valuation Through Multiples and Comparables

Alongside DCF, relative valuation offers a complementary, market-based perspective. Instead of valuing a company in isolation, it anchors valuation in how similar companies are priced.

The most commonly used multiples include:

- EV / EBITDA → Focuses on operating performance and is widely used across industries

- P / E (Price-to-Earnings) → Reflects equity value relative to net income

- EV / Revenue → Particularly relevant for high-growth or early-stage companies

- EV / EBIT → Incorporates capital intensity through depreciation and amortization

However, selecting the right multiple is only part of the process. The real challenge lies in identifying truly comparable companies.

A robust comparable analysis typically considers:

- Industry and business model

- Growth profile and scalability

- Profitability and margin structure

- Geographic exposure

- Company size and market positioning

In imperfect markets, multiples themselves fluctuate with sentiment. This means comparables reflect current market conditions—but not necessarily intrinsic value.

A Practical Example: Valuation in an Imperfect Market

Consider a company generating €1 million in Free Cash Flow, growing at 5%, with a 10% discount rate. A DCF approach suggests a valuation of €20 million.

Now suppose comparable companies trade at 12x EBITDA, implying a valuation of €24 million.

This difference does not mean one method is wrong. It reflects differences in expectations, perceived risk, and market sentiment.

Valuation, therefore, is not about choosing a single number—but about understanding a range.

Conceptually, market price fluctuates continuously, while intrinsic value evolves more gradually based on fundamentals. The gap between the two represents either opportunity or risk.

Bringing It All Together

A company’s valuation is shaped by fundamentals, expectations, risk, and market conditions—but also by how efficiently markets process information.

DCF provides a theoretical anchor. Multiples reflect market reality. Market inefficiencies explain the gap between the two.

Understanding this interaction is what allows for better decision-making.

Final Thoughts

Valuation is not about precision—it is about insight.

Markets are neither perfectly efficient nor completely irrational. They operate somewhere in between. And within that space, the ability to interpret both fundamentals and market signals becomes a true competitive advantage.

A Practical Note

In practice, robust valuation requires combining methodologies, challenging assumptions, and structuring analysis in a clear and consistent way.

Whether you are building a financial model, valuing a company, or assessing an investment opportunity, integrating DCF and comparables—while understanding market dynamics—leads to more informed decisions.

If you are currently working on a valuation or need a tailored financial model, you can explore available resources—or reach out for a more customized approach aligned with your specific objectives.